Understanding the concept of Transactional Funding For Wholesalers can be a game-changer for real estate investors. This unique financing method provides an avenue to close deals without having to use your own money or take on long-term debt.

In this competitive real estate market, being aware of all your financing options is crucial and transactional funding could be the key that unlocks new opportunities for you.

“Knowledge is power.” With that in mind, we’re about to delve into the nitty-gritty details of how transactional funding works, its advantages and disadvantages, qualifying criteria and much more!

We’ll also explore how transactional funding cost factors into your overall investment strategy.

The world of Transactional Funding For Wholesalers is vast and complex,

wouldn’t it be great if someone broke down everything you need to know?

Let’s take action and get the ball rolling! So let’s get started!

Table of Contents:

- Exploring the Concept of Transactional Funding

- How Does Transactional Funding Work?

- Advantages and Disadvantages of Transactional Funding

- Qualifying for Transactional Funding

- Using Transactional Funding for Different Real Estate Scenarios

- Alternatives To Transaction Financing

- FAQs in Relation to Transactional Funding for Wholesalers

- Conclusion

Exploring the Concept of Transactional Funding

In the world of real estate investing, transactional funding has emerged as a viable short-term financing strategy. This approach is particularly beneficial for real estate wholesalers who are looking to close deals without risking their own funds.

Transactional funding, also known as flash funding or ABC funding, is typically offered by transactional funding lenders or gator lenders. It’s commonly used in real estate transactions involving wholesalers where an end buyer is already lined up.

The Role of Key Players in Transactional Funding

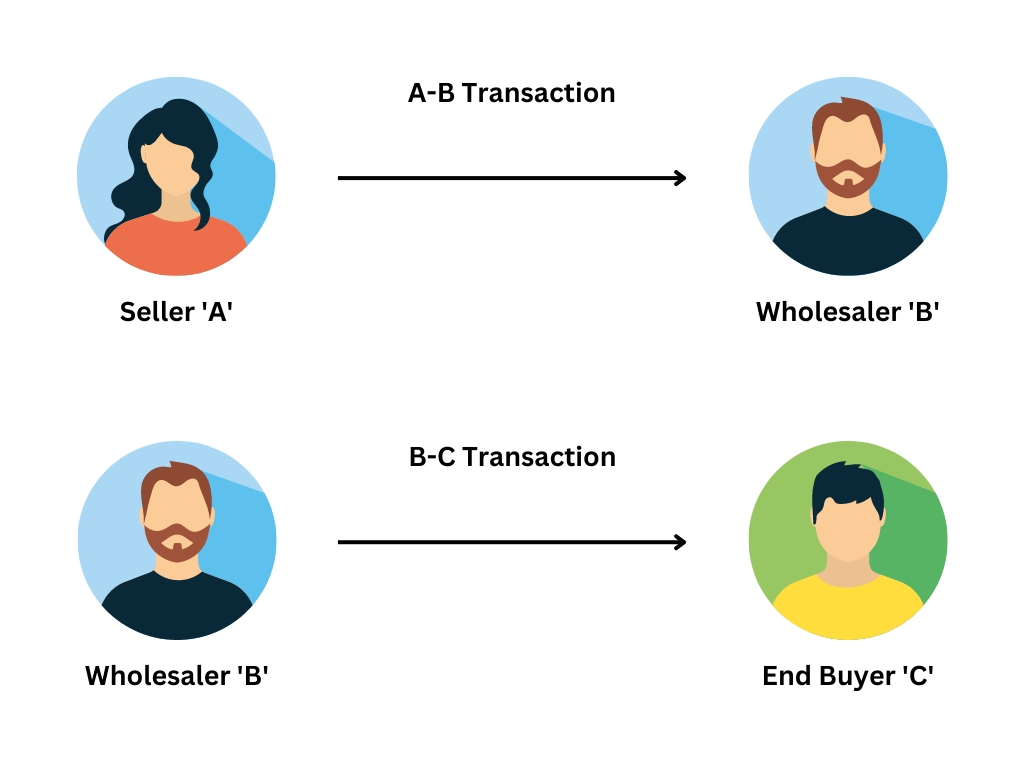

A typical transactional lending scenario involves four key players: the original owner (or initial seller), investor (or wholesaler), end buyer, and transactional lender or gator lender. Each player plays a crucial role in ensuring that the deal progresses smoothly from start to finish.

The investor commences the process by inking an agreement with the original proprietor to acquire a real estate at a determined cost. The investor then finds an end buyer willing to buy the property at a higher price on the same day or within hours after purchasing it from the initial seller.

The difference between what they pay for buying from motivated sellers and selling to qualified end buyers forms their profit margin.

Funding From Transactional Lenders

To facilitate this process, investors often turn towards gator lenders or transactional lenders. These lenders provide transactional loans covering 100% of purchase costs which enables investors not only to secure properties but also manage closing costs without any upfront fees or out-of-pocket expenses involved.

The loan amount usually equals exactly what was agreed upon during negotiations between all parties involved – no more, no less.

Transactional Lending – A Short-Term Solution

Borrowing through transactional lending offers several advantages over traditional loans including speedier approval times and fewer qualification requirements. However, it’s important for borrowers like you to understand its short-term nature before opting for such solutions.

This form of financing isn’t meant for long-term investments but rather works best when there’s a quick turnaround time expected between buying and selling properties, i.e., double closings happening within days or even minutes apart.

Transactional funding is a short-term financing strategy used by real estate wholesalers to close deals without using their own funds. Private money lenders provide loans that cover 100% of the purchase costs, allowing investors to secure properties and manage closing costs with no upfront fees or out-of-pocket expenses.

How Does Transactional Funding Work?

In the realm of real estate, transactional funding is a unique financing strategy designed to facilitate quick and seamless real estate deals, especially for wholesalers who often need funds on short notice.

The process begins with loan approval, typically within 24 hours to two days. These transactional loans are tailored for speed, allowing you to secure the necessary funds swiftly.

The next step involves purchasing the property from an initial seller using these borrowed funds. This purchase forms part one of what’s known as a double closing in real estate investing terminology.

Then comes simultaneous closing, where you sell the same property to your end buyer at a higher price on the very same day. The profits earned from this sale are used to pay back your lender immediately, completing both transactions smoothly and efficiently.

Understanding the Short-Term Nature of Transactional Funding

This form of lending is incredibly short-term – sometimes lasting only minutes or hours. That’s because transactional funding operates under the assumption that there’s already an end buyer lined up ready to buy your property once it’s purchased from its original owner (the motivated seller).

If everything goes according to plan, transactional funding allows you as a wholesaler not just to fund 100% of your purchase price but also to earn significant profits without risking any personal capital upfront.

This type of flash funding can be ideal if you’re looking for quick turnarounds in real estate deals without getting tied down by extended loan term commitments associated with traditional loans or other types of financing options available in the real estate market today.

Advantages and Disadvantages of Transactional Funding

In the world of real estate investing, transactional funding offers a unique financing solution. However, transactional funding is not without its drawbacks.

The benefits are numerous for real estate wholesalers.

Transactional lenders typically fund 100% of the purchase price, which eliminates the need to use your own capital or find additional investors. This is particularly beneficial if you’re working on multiple deals simultaneously.

Besides covering all costs associated with buying the property, transactional funding also has straightforward processing procedures, making it easier for beginners in real estate wholesaling to navigate through their first deal.

Moreover, qualifying for these loans often requires less stringent criteria compared to traditional loans – an attractive feature for those who may not have perfect credit scores or extensive investment portfolios.

Cost Implications in Transactional Funding

A key downside that needs consideration is the cost implication involved in using this type of funding. The total loan amount will include an origination fee charged by private money lenders along with higher interest rates due to short-term loan durations – some lasting just hours.

Penalties can be imposed, which could significantly increase closing costs.

Despite these potential drawbacks, many investors still consider transactional lending because they only pay back what they borrow.

In essence, transactional funding provides flexibility while minimizing risk exposure.

However, it’s essential that each investor carefully assesses whether this form of financing aligns well with their specific business model and risk tolerance level before proceeding.

Remember: While there is no single approach that applies to everyone when deciding between the various real estate financing options, understanding how each works can help make more educated decisions about which could be most suitable for individual objectives and ambitions in terms of future investments within the sector.

Transactional funding offers real estate wholesalers numerous benefits, such as 100% financing and simplified processing procedures. However, it comes with higher costs due to origination fees and short-term loan durations. Investors should carefully assess whether this form of financing aligns well with their business model and risk tolerance level before proceeding.

Qualifying for Transactional Funding

To qualify for transactional funding, real estate wholesalers need to meet certain requirements. These prerequisites are designed to ensure that there’s a qualified end buyer lined up before lending begins.

You must have an executed contract with both the initial seller and the end buyer.

This is crucial as transactional funding lenders provide funds based on these contracts. They want assurance that you’re representing a business entity and not borrowing funds for personal use.

The Importance of an End Buyer Contract

An end buyer contract plays a pivotal role in qualifying for transactional funding. Without it, getting approval from transactional funding lenders can be challenging if not impossible.

It’s important because this document provides proof that you have a motivated seller ready to sell their property and an interested party willing to buy it at a higher price.

In other words, having an executed contract with your end buyer ensures that you will be able to pay back the transactional loan within the stipulated time frame – typically when closing occurs between you (the wholesaler) and your end buyer.

If, by any chance, the deal doesn’t close or falls through due to unforeseen circumstances such as a failure in property inspection or financial issues on the part of either the original owner or the final purchaser, you might face penalties depending upon the terms set forth by your transactional funding lender.

Hence, always make sure all parties involved understand their roles clearly and contractual obligations are met diligently. This will not only secure the necessary funds but also avoid potential risks associated with defaulting on repayment commitments under this type of short-term loan arrangement, often referred to as “flash funding”.

Remember, your ultimate goal should be making profits out of real estate deals rather than just securing finances from private money lenders using the ABC funding strategy, where A refers to the initial seller (original owner), B stands for the wholesaler (you), and C represents the final purchaser (your client).

To qualify for transactional funding, wholesalers need to have executed contracts with both the initial seller and the end buyer. These contracts are crucial as they provide proof that there is a motivated seller and an interested buyer, ensuring repayment of the loan. It’s important to understand all parties’ roles and meet contractual obligations to avoid penalties or risks associated with defaulting on repayment commitments in this short-term loan arrangement known as “flash funding.”

Using Transactional Funding for Different Real Estate Scenarios

In the world of real estate investing, transactional funding is a versatile tool that can be applied to various scenarios. This type of financing isn’t just limited to double closings; it also offers solutions for real estate wholesalers who lack capital.

Transactional funding allows you to fund 100% of your purchase price, making it an ideal choice when traditional loans aren’t feasible or quick enough.

Leveraging Transaction Financing For Commercial Real Estate

If you’re involved in commercial real estate, transactional funding can prove highly beneficial. It’s especially useful when dealing with motivated sellers who are eager to close deals quickly and move on. Despite its potential benefits, transactional funding carries risks and rewards that should be carefully considered.

The key lies in understanding how transactional lending works, ensuring you have a qualified end buyer lined up, and being prepared if the deal doesn’t close.

Paying Earnest Money Deposits (EMD) With Transactional Funding

A common scenario where transactional funding comes into play is when paying Earnest Money Deposits (EMD). As a wholesaler, coming up with EMD might be challenging due to a lack of sufficient funds at hand. In such cases, transactional lenders step in providing funding.

Bridging The Gap Between Initial Seller And End Buyer

Sometimes all that stands between closing a lucrative deal is timing – getting funds from the end buyer to pay off the initial seller promptly. Here again, flash funding or ABC Funding proves invaluable by bridging this gap seamlessly without upfront fees.

Navigating Double Closings Using Transaction Loans

In situations involving double closings where one property sale depends on another’s completion – often within hours – having access to quick cash through hard money lenders offering transaction loans makes all the difference.

Transactional funding is a versatile tool in real estate investing that can be used for various scenarios, such as providing capital for wholesalers who lack funds. It allows investors to fund 100% of the purchase price when traditional loans are not feasible or quick enough. This type of financing is particularly beneficial in commercial real estate deals with motivated sellers, but it’s important to understand how transactional lending works and have a qualified end buyer lined up. Transactional funding also comes into play when paying Earnest Money Deposits (EMD) and bridging the gap between the initial seller and end buyer. Additionally, it proves invaluable in navigating double closings where timing is crucial for completing multiple property sales within hours.

Alternatives To Transaction Financing

In the world of real estate investing, there are several alternatives to transactional funding. Different financing options come with varying pros and cons, depending on individual requirements.

Let’s explore some popular financing options:

Hard Money Loans Vs. Transaction Financing

Hard money loans are a common choice for real estate investors who need quick access to capital. Unlike traditional banks or financial institutions, hard money lenders can provide funds within days instead of weeks or months.

The catch? They typically charge higher interest rates and upfront fees compared to other types of loans due to the increased risk they take on by lending based primarily on collateral value rather than borrower creditworthiness.

Private Money Loans: A Flexible Alternative?

If you have a network of wealthy individuals or private investors willing to lend you money for your real estate deals, then private money loans could be an option worth considering.

This type of loan offers flexibility in terms but often comes with higher price tags due to the personalized service and potential lack of competition among lenders.

Leveraging Home Equity: HELOCs And Second Mortgages

A home equity line of credit (HELOC) or second mortgage allows homeowners to borrow against their property’s equity. While these options offer lower interest rates than hard money loans or private lender offerings, they also put your home at risk if you fail to pay back the borrowed amount.

JV Capital: Sharing The Risk And Reward

If sharing profits doesn’t bother you much, joint venture (JV) capital might be an attractive alternative. In this arrangement, another party provides funds while sharing both risks and rewards associated with the investment project. Remember though that partnership disputes can complicate matters down the line.

Finding The Right Fit For Your Needs

All these financing methods serve different purposes and come with unique pros & cons relative to transactional funding – which is known for same-day funding without requiring any personal guarantees from borrowers. Your choice should align well with factors like purchase price, total loan amount needed, deal timeline, and exit strategy, ensuring smooth execution from initial seller contract till closing costs settlement with the end buyer.

In the world of real estate investing, there are alternatives to transactional funding such as hard money loans, private money loans, leveraging home equity through HELOCs and second mortgages, and joint venture capital. Each option has its own advantages and disadvantages depending on factors like purchase price, loan amount needed, timeline, and exit strategy. It’s important to choose the financing method that aligns best with your specific needs for a smooth execution of your real estate deals.

FAQs in Relation to Transactional Funding for Wholesalers

What is transactional funding for wholesaling?

Transactional funding is a short-term loan used by real estate wholesalers to fund their deals.

Why would you use transactional funding?

Because it allows wholesalers to quickly close deals without using their own money or credit.

Conclusion

In conclusion, Transactional Funding For Wholesalers offers a short-term financing solution for real estate wholesalers to quickly close deals and profit from their transactions.

With the involvement of key players such as the original owner, investor, end buyer, and private money lender, this funding method allows wholesalers to leverage executed contracts with qualified end buyers to secure the necessary funds for their deals.

While transactional funding provides advantages like fast approval and same-day funding, it also comes with higher interest rates and potential penalties if a deal falls through.

It’s important for wholesalers to carefully consider the cost implications before opting for this type of financing.

Alternatives such as hard money loans may offer lower interest rates but come with longer loan terms and upfront fees.